When it comes to saving and investing money, few people have the confidence and determination to stick to their goals and maintain the discipline needed to put away large sums of money or make the most of their savings.

That’s where FinTech (Financial Technology) apps like Chip comes in. Using its AI algorithms, and regular savings and investment goals directed by the user, Chip automatically makes savings in a way that doesn’t impact your ability so spend money.

Over 250,000 people have downloaded Chip, and it has a high user review score of 4.1 out of 5 stars, showing that it is widely accepted as a useful app that brings good results for most of its users.

There are a few other platforms for Chip to compete with, none bigger than the Moneybox app, which has proven to be extremely popular with the public.

Well, I’m here to find out how well that stacks up. In my Chip savings App review, I will be digging deep into exactly what is offered, at what cost, and how much value is provided for the average user, where you have £1 to save, £1000 or a million.

I found some very interesting results, and they may surprise you on how the app works for the users it targets — young millennials looking to save and invest a bit of extra cash.

Chip savings review — The real deal

Setting up the app was fairly straightforward, and I had no problems connecting my bank account, but I have seen numerous reports of accounts not being recognized and a relatively slow customer service response to these issues.

In my Chip savings App review, I tested out the free trial of ChipAI, having access to most features of the app aside from ISAs and some of the more complex investment funds. I found the app to be well-designed and intuitive, with a lot of helpful information available, without cluttering the interface.

It was definitely the best out of the other FinTech saving and investment apps I’ve tired, but unfortunately the actual saving and investment experience was a little less pleasant.

I found the fees to be relatively high compared to other options, where the investment fees were particularly expensive.

The investment fund options were also slimmer than most alternative apps, offering only three different “types” of investment portfolio with the ChipAI membership, while the rest were locked behind the more expensive ChipX membership tier.

This is pretty needless, as they are making money out of you either way, so I don’t understand their choice to lock additional investment options behind a higher subscription tier.

Pros

- Very clean interface

- Highest APR Easy-Access account I can find

- Great savings-encouragement tools

- Very informative about deposits and withdrawals

- Automatic saving with paid account

- ISA and GSA account available with highest account tier

Cons

- 50p withdrawal fee (on more than 1 withdrawal per 28 day period)

- High investment management fees

- Most good features behind paywall

- Free account does not offer automated savings

What Chip offers savers

Chip allows you to highly customize the way you save, based on how comfortable you are financially. There are 5 different saving levels you can choose from which each save more aggressively than the last.

This lines up perfectly with the Goals feature, which allows you to set personalized savings targets for events or purchases. The app will even help you pick an achievable target date based on how the AI thinks you will do.

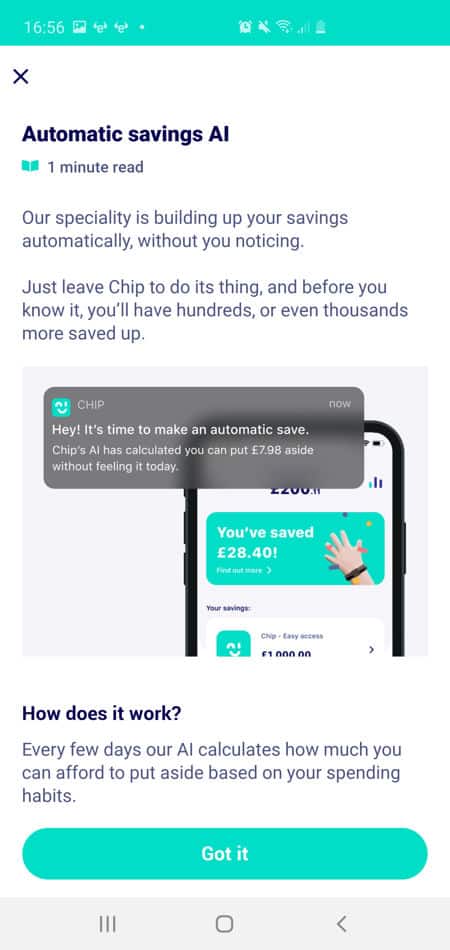

Chip is also incredibly informative when it comes to the process of saving, and will inform you, when it’s going to save via notifications and a quicky chat bot which notifies you with animated gifs. You always have the option to cancel a planned savings deposit if you feel like you want to skip a day.

I found Chip to have very good interest rate saving accounts, where the highest interest offered was 0.7% APR, which can be earned on up to £30,000. A one-time friend referral system also allows a new user to access a savings account paying 1.25% APR up to £5,000.

How does that compare?

The downside is almost all of the good features that the Chip App offers are behind paywalls, and this wouldn’t matter too much if the goal of saving wasn’t to save money when competitors offer some of these features for free.

One feature of Chip I really disliked was the £0.50 withdrawal fee on more than one withdrawal over a 28-day period. This is highly inconvenient as it turns saving into a liability if you regularly need to pull out money for certain expenses.

You are essentially paying money to shuffle your own money back and forth. Compared to other savings apps that offer free, unlimited withdrawals and don’t charge you to access your own money, this was one of the biggest let downs of Chip in my opinion.

Chip also didn’t offer automatic savings with its free account, requiring you to manually deposit money to save it, which ultimately defeats the purpose of using an AI savings app in the first place.

How to invest with Chip

Chip offers a small range of investment tools and is partnered with BlackRock, which provides their investment services. They offer three portfolios to choose from that each has a different risk level to suit your investment style and appetite.

A further 3 funds are locked behind the ChipX tier, and offer emerging markets, green energy, and ethical options.

Currently, you can’t simply add funds to your investments from your savings on Chip, you need to deposit any savings back into your main bank account, and then deposit them into your investment portfolio with the app.

It might seem weird and convoluted, and that’s because it is. Chip states that they are looking to address this in the future and allow you to automatically invest from your savings pot.

Is opening a Chip account worth it?

BlackRock’s investment history is fairly positive, so I don’t have too much of an issue with the expected returns of the three main portfolios offered, Cautious, Balanced and Adventurous. Their other portfolios varied much more in returns, from almost 0% return, up to 12%.

What I have a problem with is their pricing. There is a 0.22% fund management fee charged by BlackRock, and you will need to pay a platform free to Chip on top, which will depend on your subscription tier.

ChipAI will cost you a 0.75% annual fee while ChipX will cost 0.25% annually. These fees together will eat a significant chunk from your investment gains, and with the added cost of the subscription for these tiers, I don’t see great value in the investment options offered.

For example, you have £5000 invested with ChipAI, it will cost you £37.50 for the Chip 0.75% fee, £11 for the BlackRock fee, and £19.50 for the subscription. In total it would cost you £68/year to maintain £5000, which is a total loss of 1.4%

Compared to other FinTech investment and savings apps, Chip seems to be on the more expensive side in terms of management fees as well, so I would not recommend it for investing.

Is Chip safe to use?

When Chip debits your bank account, the saved money is placed into a Barclays ring-fenced account and stored as e-money. Money held in this account is not covered by the Financial Services Compensation Scheme (FSCS) but is regulated by the Financial Conduct Authority (FCA).

Chip says this money is not at risk and not used in trading activities, therefore its safe, while not being covered by the £85,000 FSCS guarantee.

If you keep your money in a Chip interest or investment account, you will be fully covered by the FSCS up to £85,000, so this is a safer place to keep it in my opinion.

In terms of digital security, Chip boasts 128-bit encryption software as a security feature to protect your data. This is reassuring, as there have been a series of high-profile hacking incidents in recent years, resulting in masses of personal data being lost or stolen.

I would consider Chip to be about as safe as any of the other FinTech saving and investing apps.

How much does Chip cost?

Chip has three different tiers of subscription, and each one offers the features of the previous, providing more features than the last.

It’s worth saying that Chip seems to have the most additional costs related to its services with the least number of features offered for its free service compared to other providers.

Chip Lite

This tier is generally free but can incur costs detailed below.

- Free and standard to use

- Can save you up to £100/28 days before charging a £1 fee per month this limit is exceeded

- 0.7% interest in Easy Access savings account up to £2000

- 1.25% bonus in Chip+1 account on funds up to £2,000

ChipAI

This tier costs £1.50/28 days and includes everything in the previous tiers. There is a 28 day free trial available.

- Automatic savings AI

- Access to investment accounts (Cautious/Balanced/Adventurous)

- 1.25% bonus in Chip+1 account on funds up to £10,000

- 0.7% interest in Easy Access savings account up to £30,000

- Access savings tactics such as Pay Day Put Away and goals.

ChipX

This tier costs £3/28 days and includes everything in the previous tiers.

- Access additional investment fund themes, such as ethical funds or emerging markets

- Access to Stocks and Shares ISA (Individual Savings Account) and GIA (General Savings Account)

- First access to new features

Common Questions about Chip Savings

How long does it take to withdraw my money from Chip?

Depending on the type of your account, you can expect same-day withdrawals (before 5PM) with an instant-access account, and up to 3 days with other interest accounts.

Can you withdraw money from Chip?

Yes, it’s straightforward to withdraw money from your Chip account. Just bear in mind that it can take a few days for the money to make its way to your linked bank account – though this is the norm for any general investment account.

Is Chip a good investment?

Unless you have some experience with investing, apps like Chip Savings generally offer a great service that allows for hands off investing.

Conclusion

Unfortunately, while the interface and concept of Chip is fairly inviting, the implementation is relatively poor in my opinion.

There are a bunch of potentially great features, but the cost and fact that they are behind paywalls, or have restrictive limits, is disappointing.

If you have a small balance, the membership fees and maintenance fees will definitely give you a net negative result on any savings made, and even if you have a lot of money to save, there’s a limit to how much money the rate applies to.

Overall, the app is okay to use if you really struggle to put away and money, and you are willing to pay a fee to have the app manage your money for you, but the interest retuns will be wiped out and any investment returns you make will be significantly reduced due to management fees.

I would personally skip this one, as I believe there are better options out there.